I'm a content writer with 5+ years of experience creating engaging blog content and digital assets. I turn research into stories that drive traffic, boost visibility, and keep audiences coming back.

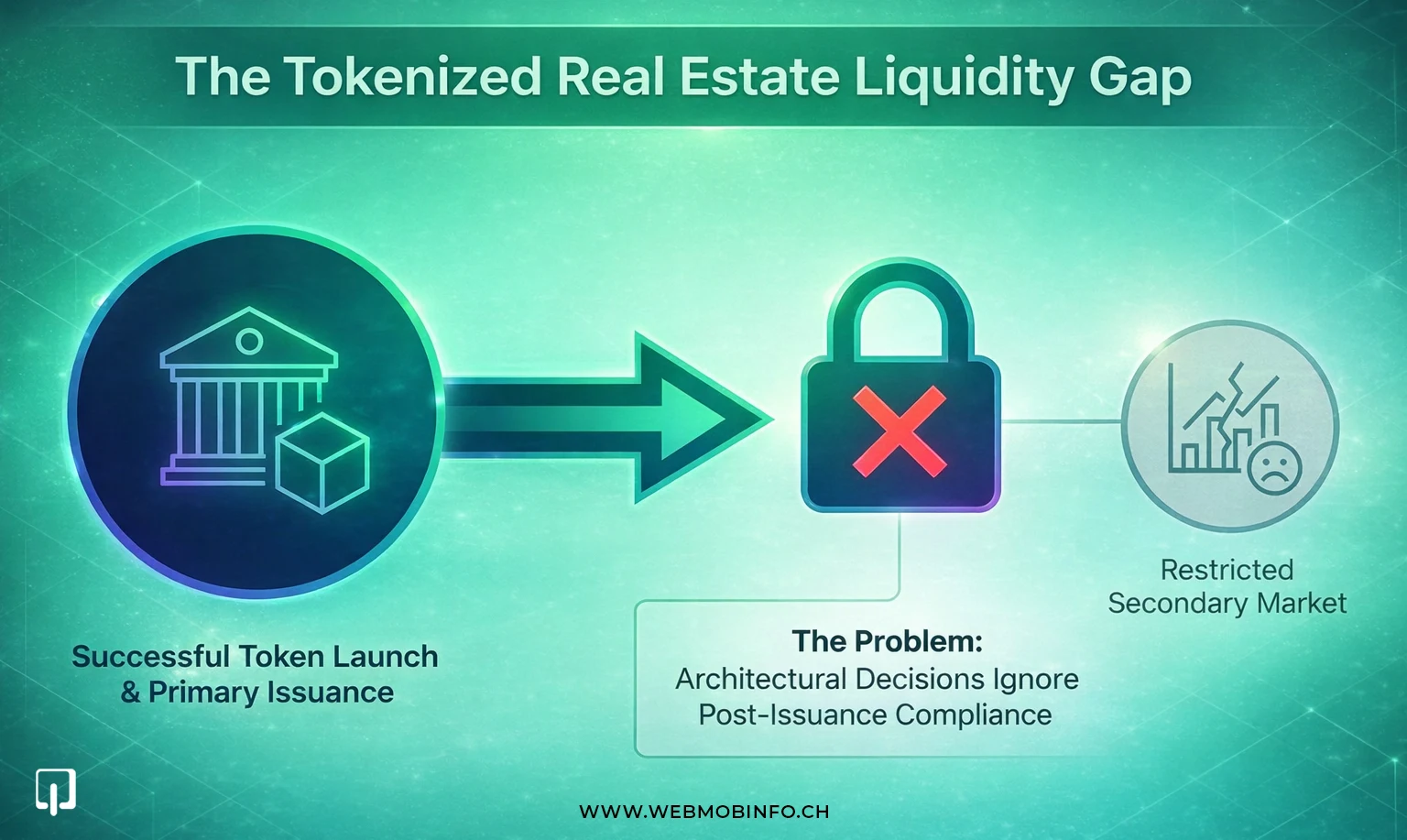

Real estate tokenization has matured beyond proof-of-concept platforms. Asset issuers today are able to tokenize property interests, onboard investors, and complete compliant primary issuance. However, many tokenized real estate projects face a critical limitation after launch: restricted or non-existent secondary market liquidity.

In most cases, it is the result of architectural decisions made during the tokenization phase. Secondary markets for real estate tokens require a compliance-first, permissioned design that differs significantly from open crypto trading environments.

This blog explains how compliant secondary markets for real estate tokens are architected, which technical and compliance components are required, and how liquidity can be enabled without compromising regulatory obligations.

Tokenization introduces digital ownership, fractionalization, and programmable settlement. These benefits are fully realized only when token holders can legitimately transfer or trade their positions after issuance.

Without proper secondary market liquidity solutions:

In real estate tokenization, liquidity cannot be addressed as an afterthought. Unlike cryptocurrencies, real estate tokens represent regulated assets that must comply with securities laws, investor eligibility rules, and jurisdiction-specific regulations.

As a result, secondary market liquidity must be designed at the architectural level, not layered on later through external marketplaces.

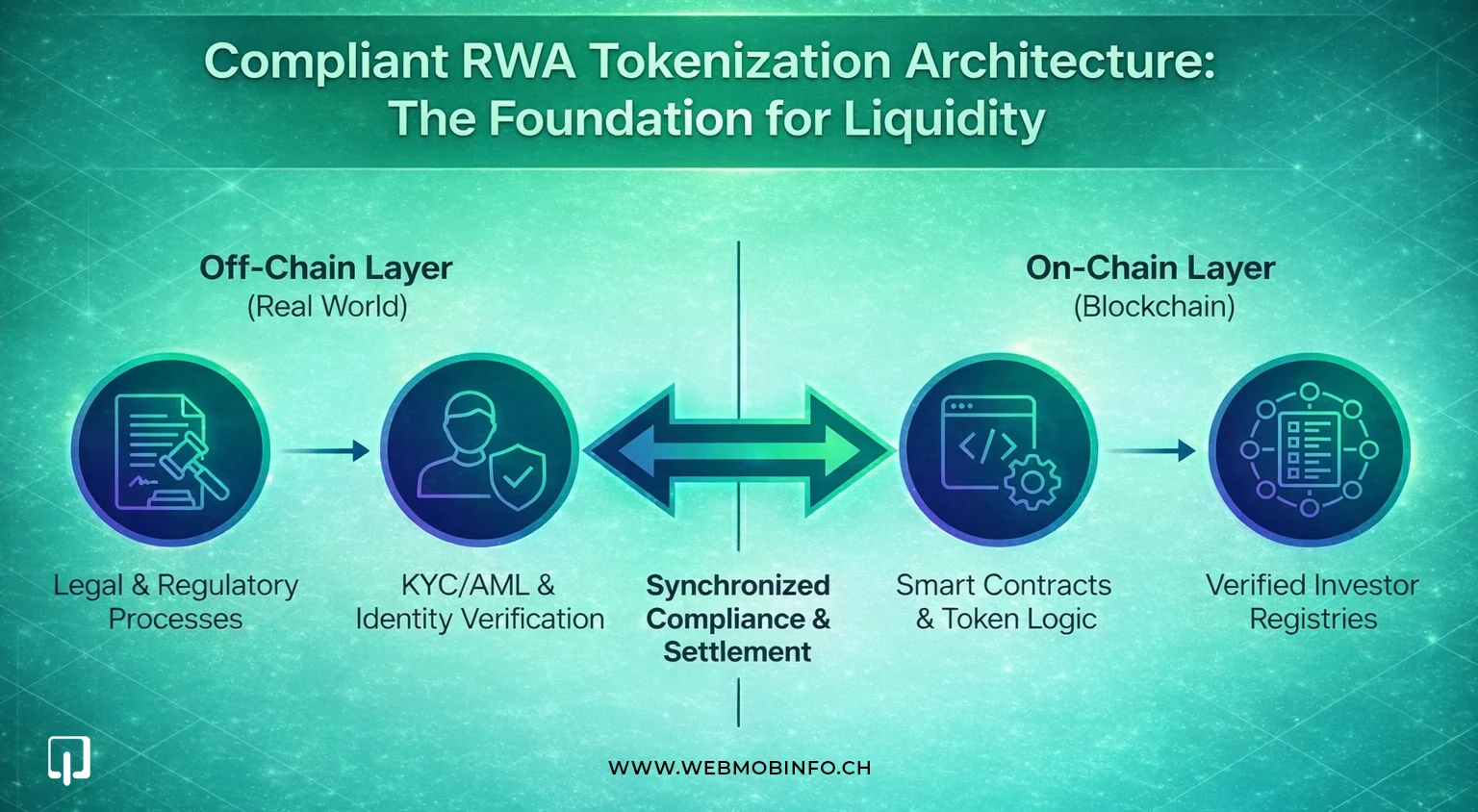

A compliant secondary market begins with a well-defined RWA architecture that separates responsibilities across on-chain and off-chain systems.

Real estate tokenization platforms typically rely on:

The interaction between these layers determines whether secondary trading can be supported in a compliant manner.

Smart contracts define how tokens behave. In the context of secondary markets, they must be capable of enforcing:

Registries maintain lists of verified investors, approved wallets, and compliance attributes. These registries are referenced by smart contracts during each transfer attempt, ensuring that compliance checks are enforced automatically.

This architectural approach is central to effective RWA tokenization development services, where secondary trading requirements are accounted for from the initial design stage.

This level of architectural rigor is increasingly necessary as the tokenized real estate market is projected to grow from approximately USD 3.5 billion in 2024 to nearly USD 19.4 billion by 2033, increasing the need for scalable, compliance-ready secondary market infrastructure.

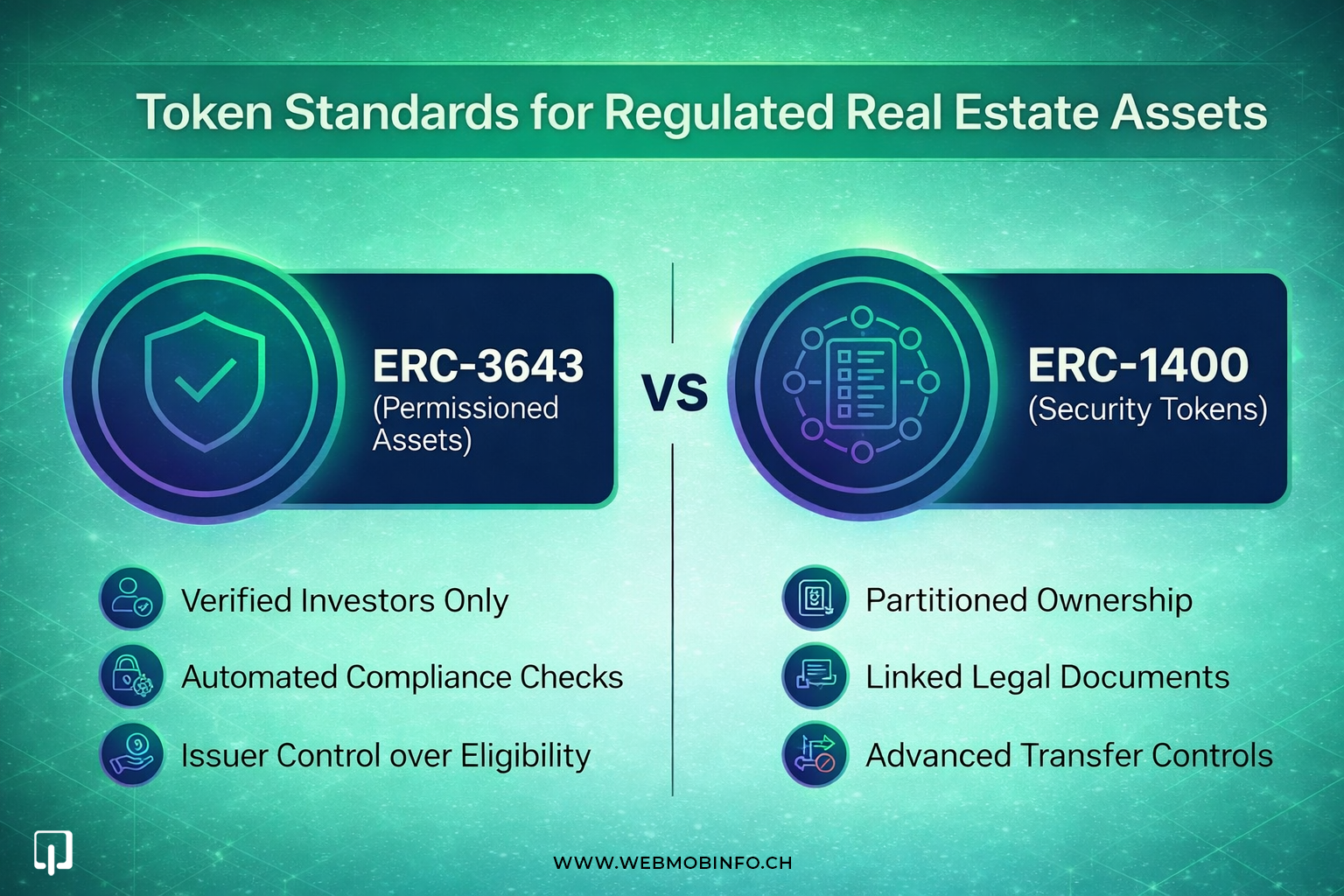

Token standard selection directly affects a project’s ability to support compliant secondary markets.

ERC-3643 is designed for regulated tokenized assets. It enables permissioned transfers by embedding compliance checks directly into the token contract.

With ERC-3643:

This makes ERC-3643 well-suited for real estate tokens that must support secondary trading while remaining compliant with regulatory requirements.

ERC-1400 provides a broader framework for security tokens, including features such as:

An ERC-1400 token implementation is often selected when issuers require structured ownership models or need to reflect complex legal arrangements within the token design.

Tokens issued without built-in transfer controls often face difficulties when secondary markets are introduced. Retrofitting compliance into existing tokens increases technical complexity and regulatory risk.

Selecting the appropriate standard during the design phase ensures that secondary market liquidity solutions can be implemented without restructuring the token architecture.

Compliance is not a peripheral requirement in real estate tokenization. It is the foundation on which secondary markets operate.

Every participant in a compliant secondary market must undergo identity verification and risk screening. KYC/AML integration for tokenized assets ensures that:

These processes typically occur off-chain but are enforced on-chain through smart contract logic and registries.

On-chain identity verification solutions link verified identities to blockchain addresses. Instead of storing sensitive data on-chain, cryptographic references or proofs are used to confirm investor status.

This approach allows smart contracts to verify eligibility during each transaction while preserving data privacy and regulatory compliance.

Real estate assets are tied to specific legal jurisdictions. Secondary market architecture must account for:

A properly designed system ensures that these rules are enforced automatically at the transaction level.

Secondary markets for real estate tokens operate differently from open crypto exchanges.

In a compliant environment, access to secondary trading is controlled. Typical flows include:

This structure ensures that all trades comply with legal and regulatory obligations.

Secondary trades must synchronize:

Architectural alignment between these systems prevents inconsistencies between digital tokens and legal ownership documentation.

Smart contracts play a critical role in blocking unauthorized peer-to-peer transfers. Transfer functions are designed to fail when compliance conditions are not satisfied, ensuring that all secondary activity remains within approved channels.

Liquidity in real estate token markets must be controlled, not unrestricted.

Secondary markets may be implemented as:

Each model allows liquidity while maintaining oversight and regulatory alignment.

Liquidity can be supported through:

These mechanisms provide price discovery and exit options without exposing the asset to regulatory violations.

Institutional participants require predictability, transparency, and compliance assurance. Secondary market liquidity solutions must therefore be designed to meet institutional standards for custody, reporting, and governance.

As blockchain ecosystems diversify, real estate tokenization projects may consider multi-chain deployments.

Cross-chain environments introduce complexity in:

Without careful design, these challenges can compromise regulatory compliance.

To support cross-chain real estate liquidity, systems must ensure that:

This typically requires shared registries or coordinated compliance layers that operate across networks.

Several recurring issues limit secondary market viability:

These mistakes are architectural in nature and can be avoided with a compliance-first approach.

Webmob designs real estate tokenization platforms with secondary market requirements considered from the outset. The focus is on building a complete architecture that supports regulated post-issuance trading, rather than treating liquidity as a separate layer.

This approach involves:

By aligning smart contract design, compliance enforcement, and trading workflows, Webmob enables secondary market participation while maintaining regulatory consistency throughout the asset lifecycle.

Secondary market liquidity for real estate tokens is not achieved through exposure or scale. It is the result of deliberate architectural design.

Compliance-aware token standards, identity integration, permissioned trading flows, and synchronized settlement systems form the foundation of sustainable secondary markets.

As real estate tokenization continues to evolve, projects that prioritize architecture and compliance will be better positioned to support regulated secondary trading and long-term market participation.

Let’s discuss and plan how we can accelerate your growth. Fill out this form and take the first step towards constant advancement.

We will respond to you within 24 hours.

Access to dedicated product specialists.

.webp)