I'm a content writer with 5+ years of experience creating engaging blog content and digital assets. I turn research into stories that drive traffic, boost visibility, and keep audiences coming back.

Saudi Arabia’s fixed-income market is undergoing a structural shift. Tokenized Sukuk in Saudi Arabia is no longer a theoretical concept. It is being tested, regulated, and scaled through CMA and SAMA sandboxes, with real money flowing through digital Sharia-compliant instruments. The convergence of blockchain infrastructure, permissioned token standards like ERC-3643, and national real-estate tokenization pilots is creating the technical and regulatory foundation for a new generation of Islamic bonds.

For institutions and developers looking to participate in this evolution, understanding the architecture behind smart Sukuk structuring, the regulatory frameworks governing tokenization platform development in Riyadh, and the compliance requirements for Sharia-compliant digital bonds is no longer optional. It is essential.

This article provides a comprehensive breakdown of how blockchain is modernizing Islamic bonds in KSA, the role of Vision 2030’s Financial Sector Development Program (FSDP), and what it takes to build compliant, production-grade tokenized Sukuk platforms.

Saudi Arabia’s sukuk market serves as the backbone of its domestic fixed-income system. The National Debt Management Center (NDMC) runs a regular local-currency sukuk issuance program across multiple maturities, and both sovereign and corporate sukuk are central to Vision 2030’s fiscal strategy. The goal is clear: diversify funding away from oil revenues while deepening local capital markets.

The Financial Sector Development Program (FSDP), launched in 2017 as a core Vision 2030 realization program, explicitly targets a diversified and effective financial sector. Its pillars include:

· Enabling financial institutions to support private-sector growth

· Expanding capital markets, including debt instruments like sukuk

· Promoting fintech and digital payments, which creates direct policy space for tokenized sukuk

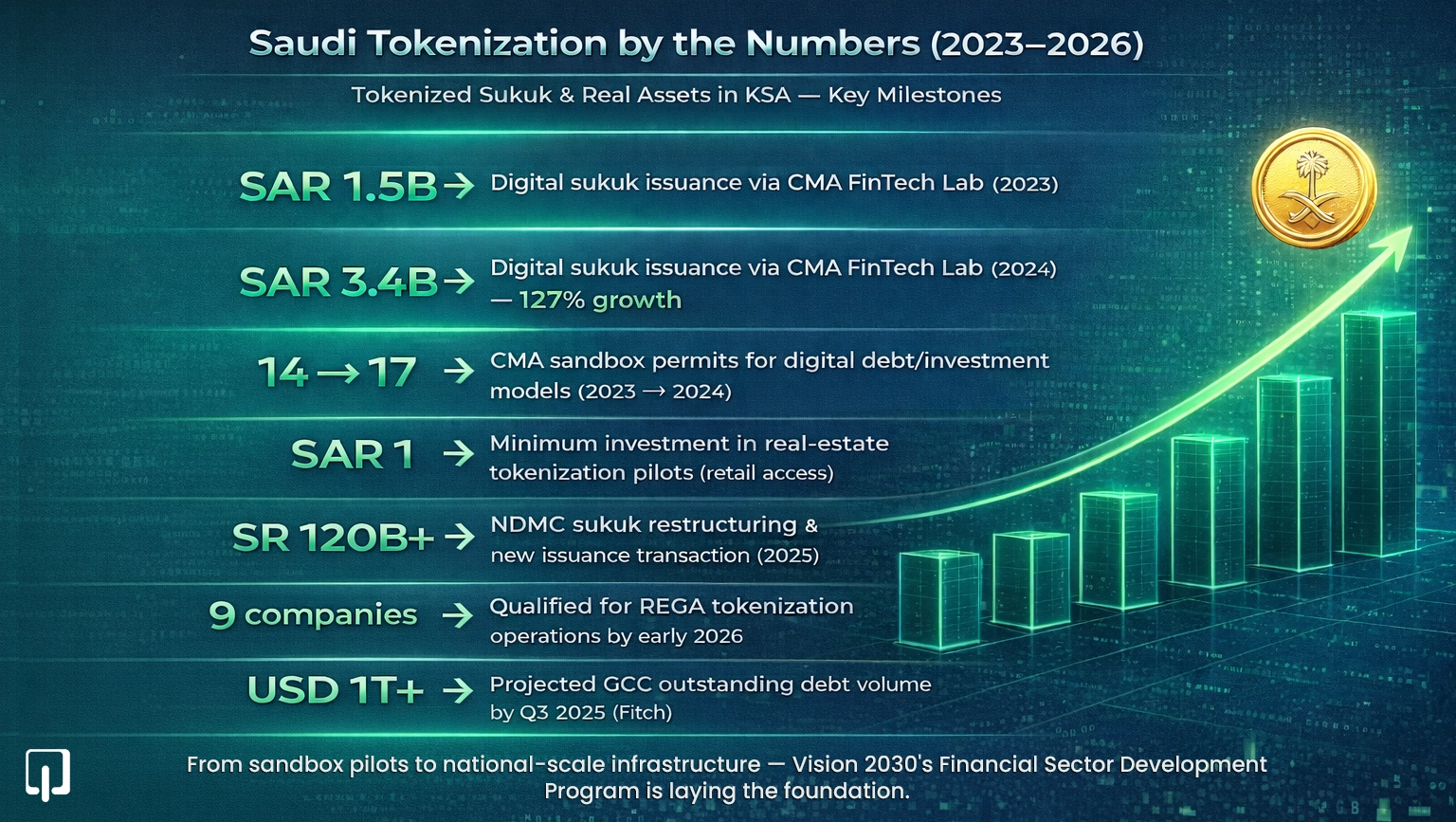

In 2025, the NDMC executed a sukuk restructuring and new issuance transaction totaling over SR 120 billion (approximately USD 32 billion). This included early redemption and re-issuance across multiple long-dated tranches, reinforcing the sheer scale of the sukuk ecosystem. At this volume, even marginal efficiency gains from tokenization translate into significant cost savings and risk reduction.

The Capital Market Authority (CMA) regulates securities in Saudi Arabia, including sukuk. It operates a FinTech Lab that allows digital-asset pilots, such as tokenized debt and sukuk, within a controlled framework. Public distribution of security tokens remains restricted, with tokenized instruments generally confined to sandbox or private-placement structures subject to CMA approval.

Here is the most concrete evidence of progress:

· Sukuk issuance through CMA’s experimental “debt offering and investment” models reached approximately SAR 3.4 billion in 2024, up from SAR 1.5 billion in 2023

· The number of permits for these models increased from 14 to 17 during the same period

· CMA-endorsed sandbox platforms use SPVs and smart legal contracts to keep offerings within existing securities law

· Minimum ticket sizes have dropped to as low as SAR 1 for retail investors in certain pilots

White & Case’s 2025 analysis describes Saudi Arabia’s approach as “measured.” CMA supervises digital securities activity through its FinTech Lab, where tokenized sukuk and other Sharia-compliant instruments can be piloted, but broad public security-token distribution is still constrained pending fuller regulatory frameworks. This stance balances Vision 2030’s innovation goals with investor protection and Sharia governance.

While CMA governs the securities side, the Saudi Central Bank (SAMA) runs a separate regulatory sandbox for innovative financial products. This sandbox explicitly includes blockchain-based solutions and digital currencies, and it provides temporary regulatory permissions, close supervisory engagement, and a pathway to full licensing after successful testing.

Key characteristics of SAMA’s sandbox approach include:

· Real customers can be engaged in a live environment, but under defined limits

· Cybersecurity and compliance requirements are stringent at every development stage

· Graduates of the sandbox can pursue full licensing once they demonstrate compliance and consumer protection

Industry commentators in early 2026 describe an expected dedicated stablecoin sandbox with specific focus areas including real-estate tokenization, cross-border trade finance, remittances, and securities settlement. This signals regulatory intent to use token-based instruments for real-world settlement use cases.

Together, SAMA’s sandbox and prospective stablecoin guidance define the settlement and payments layer upon which tokenized sukuk ecosystems are likely to run: compliant, identity-linked, and tightly monitored digital money and ledger infrastructure.

Saudi real-estate tokenization has moved beyond pilot status into national infrastructure, establishing patterns that sukuk tokenization can follow.

Saudi Arabia’s Real Estate Registry (RER), under the Real Estate General Authority (REGA), has deployed a blockchain-based asset tokenization platform in partnership with SettleMint and local IT provider Inspire for Solutions Development. This platform overlays smart contracts and blockchain orchestration on top of the national property registry to support digital ownership transfer and fractionalization of real-estate titles.

A 2025 pilot transaction between the National Housing Company and multiple investors demonstrated the first tokenization of a real-estate title deed on this infrastructure. Settlement times dropped from weeks to minutes. By early 2026, the first tokenized deed had been issued, and nine companies were qualified within the experimental environment to conduct tokenization operations, with no minimum investment requirement during the pilot phase.

In parallel, Saudi Arabia launched a regulated, sandbox-stage real-estate tokenization pilot through droppRWA (a droppGroup subsidiary) and RAFAL Real Estate Development. This program tokenizes select high-end properties in Riyadh and allows citizens to buy fractional shares with a minimum investment as low as 1 Saudi Riyal. Tokens represent proportional entitlement to rental income and capital gains.

These design choices, extreme fractionalization, sandbox-limited secondary markets, and full regulatory visibility, mirror the direction tokenized sukuk could take for retail or quasi-retail distribution, especially for real-estate-backed sukuk structures.

Sukuk are inherently well-suited to tokenization. They are typically backed by identifiable assets, have clearly defined cash-flow waterfalls, and follow fixed distribution schedules. Tokenization preserves these features by representing each beneficial unit of the SPV’s asset interest as a digital token, while smart contracts orchestrate profit distributions, principal redemptions, and event-driven actions.

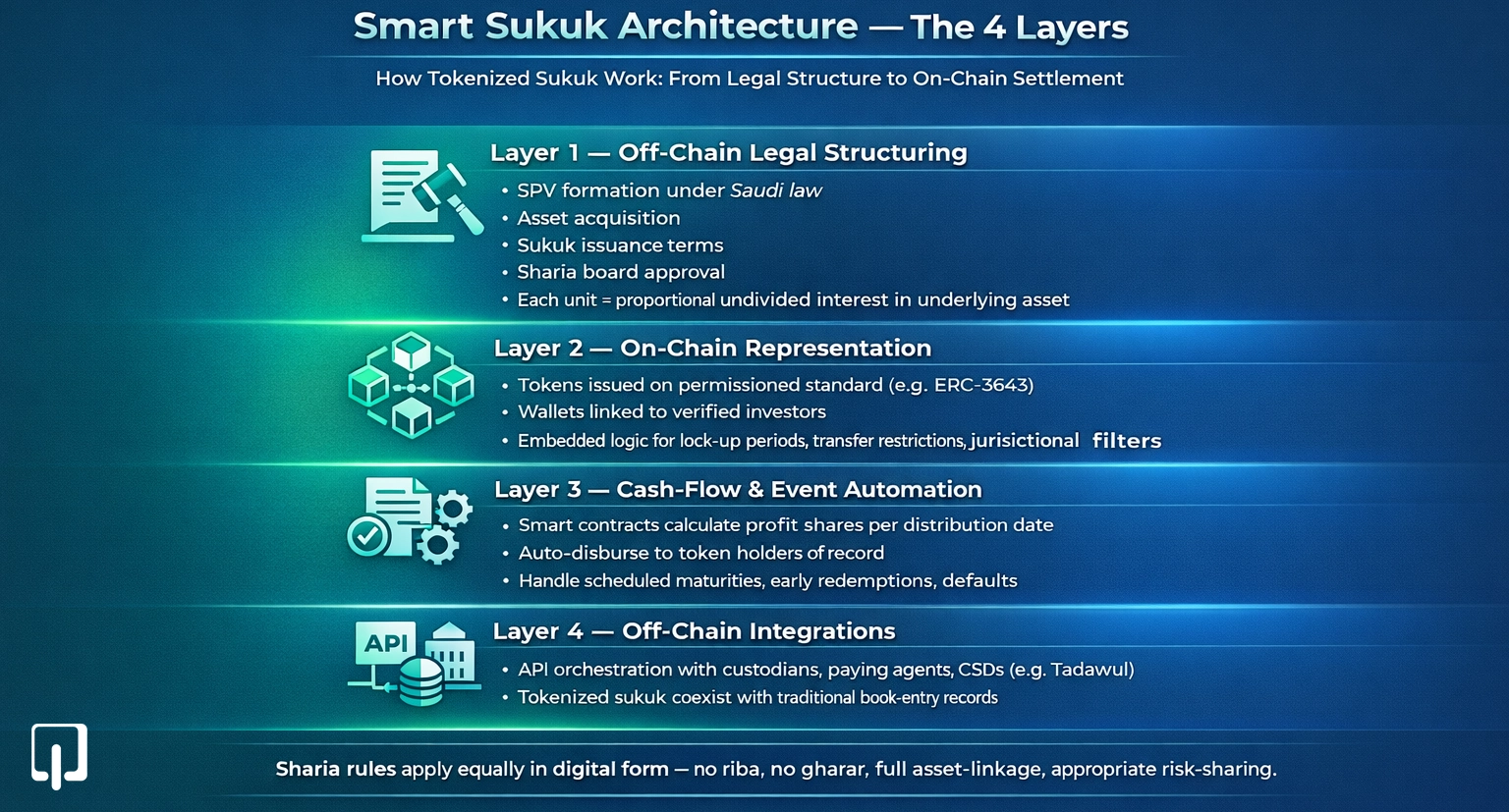

A typical smart Sukuk structuring architecture for KSA includes four layers:

· Off-chain legal structuring: SPV formation under Saudi law, asset acquisition, sukuk issuance terms, and Sharia board approval. Each sukuk unit maps to a proportional undivided interest in the underlying asset.

· On-chain representation: Tokens issued on a permissioned standard (such as ERC-3643), with each wallet linked to a verified, eligible investor. Embedded logic handles lock-up periods, transfer restrictions, and jurisdictional filters.

· Cash-flow and event automation: Smart contracts calculate profit shares on each distribution date and disburse funds to token holders of record. Event modules handle scheduled maturities, early redemptions, and defaults.

· Off-chain integrations: Orchestration with custodians, paying agents, and CSDs (e.g., Tadawul’s post-trade infrastructure) through APIs, allowing tokenized sukuk to coexist with traditional book-entry records.

In Sharia terms, the usual constraints apply equally in digital form: no interest (riba), no excessive uncertainty (gharar), asset-linkage, and appropriate risk-sharing. On-chain structures must faithfully reflect underlying Sharia-compliant contracts such as ijara, mudaraba, wakala, and murabaha.

ERC-3643 (T-REX) is an Ethereum-based token standard specifically designed for regulated security tokens and real-world assets. It extends ERC-20 with on-chain identity and compliance enforcement.

Although public documentation does not yet show Saudi regulators naming ERC-3643 specifically, its design aligns well with CMA/SAMA expectations. KYC/AML and investor-type restrictions map onto CMA requirements, the permissioned ecosystem is consistent with CMA’s measured stance on digital securities, and full auditability supports both securities governance and religious oversight.

For a tokenization platform development in Riyadh, ERC-3643 or an equivalent permissioned standard would be the natural choice for structuring Sharia-compliant security tokens, with Sharia-specific rules implemented in the compliance modules.

Tokenized sukuk and real-estate instruments in KSA will almost certainly run on permissioned or permissioned-token infrastructures. A typical Saudi bank-centric architecture would involve:

· A consortium or private network where banks, CSDs, and key market infrastructures operate validator nodes, and regulators have observer or read-only access

· Permissioned tokens (ERC-3643-like) representing sukuk units and property fractions, with all wallets mapped to KYC’d customers

· Integration adapters to banks’ core systems, payments infrastructure, and SAMA’s settlement mechanisms for seamless synchronization

This architecture ensures that tokenization works within, rather than around, existing control frameworks. For a deeper look at how enterprise blockchain development supports regulated environments, the design patterns are similar across banking and capital-market use cases.

Tokenized Islamic products in the GCC are increasingly paired with AI-enabled Sharia-compliance tools and automated lifecycle controls. Fitch Ratings highlights the emergence of these tools alongside tokenized sukuk and blockchain-based settlements as part of a broader digital transformation in GCC Islamic capital markets.

Automated compliance for smart Sukuk in Saudi Arabia could include:

· Pre-issuance checks: On-chain representation of Sharia board approvals, making it impossible to deploy a sukuk token that deviates from signed legal documentation

· Transfer-rule engines: Compliance modules preventing prohibited transfers to non-eligible investors, certain jurisdictions, or wallets that have lost KYC status

· Continuous monitoring: AI/analytics scanning on-chain patterns and off-chain KYC data for anomalies, feeding into both Sharia boards and compliance teams

Smart contract auditing for Islamic finance must also verify code-Sharia consistency (ensuring on-chain logic reproduces profit-sharing formulas exactly as approved), compliance enforcement correctness, and cyber-resilience meeting SAMA sandbox standards.

Fitch projects that tokenization and digital sukuk will transform GCC capital markets in the medium-to-long term, with outstanding regional debt volumes surpassing USD 1 trillion by Q3 2025. Tokenization adds granular, real-time data that can feed predictive models for sukuk pricing and liquidity.

In a Saudi context, predictive analytics for Sukuk pricing could draw from:

· On-chain transaction data: Price, size, and frequency of tokenized sukuk trades for modeling liquidity premiums

· Investor-segment data: Aggregated behavior of retail vs. institutional, domestic vs. foreign investors under CMA’s identity frameworks

· Macro and policy signals: NDMC issuance calendars, Vision 2030 project timelines, and FSDP metrics influencing supply-demand conditions

These models support issuance strategy, dynamic pricing, and risk management, provided regulators are comfortable with the associated data use.

Building a production-grade tokenized Sukuk platform requires deep expertise across blockchain architecture, smart contract development, regulatory compliance integration, and enterprise-grade security. Webmob, as a full-stack software development company, brings the technical capabilities needed to build permissioned blockchain systems, implement ERC-3643-based token standards, develop automated Sharia compliance modules, and integrate with existing banking and settlement infrastructure.

Whether the requirement involves white-label real estate investment platforms, SAMA-compliant ledger solutions, or end-to-end smart Sukuk structuring platforms, Webmob’s development teams can architect and deliver solutions that meet the stringent standards set by CMA and SAMA sandboxes.

Tokenized Sukuk in Saudi Arabia is transitioning from controlled pilots to scalable infrastructure. CMA’s FinTech Lab has facilitated SAR 3.4 billion in digital sukuk issuance during 2024, SAMA is shaping the settlement rails through its sandbox, and national registries are being modernized to host tokenized ownership records. The convergence of permissioned blockchain architecture, RWA tokenization standards like ERC-3643, and automated Sharia compliance monitoring creates a robust foundation for the next phase of Islamic capital markets. For institutions, developers, and financial technology firms, the window to build compliant tokenization platforms aligned with Vision 2030 and the Financial Sector Development Program is open now. The technical and regulatory groundwork has been laid, and the organizations that invest in smart Sukuk structuring and tokenization platform development in Riyadh today will be positioned to serve this market as it scales from sandbox to production.

Tokenized Sukuk are Sharia-compliant digital bonds represented as blockchain-based tokens. Each token corresponds to a proportional ownership interest in an underlying asset or SPV, enabling fractional ownership of Sukuk through digital infrastructure regulated by CMA and SAMA.

The CMA FinTech Lab allows digital-asset pilots, including tokenized debt and sukuk, within a controlled framework. In 2024, sukuk issuance through its experimental models reached approximately SAR 3.4 billion, with 17 active permits for digital debt and investment platforms.

ERC-3643 (T-REX) is an Ethereum-based token standard for regulated security tokens. It enforces on-chain identity verification, KYC/AML compliance, and transfer restrictions at the token level, making it well-suited for structuring Sharia-compliant security tokens within Saudi regulatory frameworks.

The FSDP targets a diversified financial sector with expanded capital markets, increased non-cash transactions, and broader investor access. Tokenized sukuk serve these goals by enabling fractional ownership, improving secondary-market liquidity, and reducing issuance costs through automation.

SAMA runs a regulatory sandbox for blockchain-based financial products, including digital currencies and settlement solutions. Its sandbox defines the settlement and payments layer upon which tokenized sukuk ecosystems are likely to operate, with strict cybersecurity and compliance requirements.

Yes. CMA-endorsed sandbox platforms have enabled minimum investments as low as SAR 1 for retail investors in certain real-estate tokenization pilots. Similar fractional ownership models are being applied to sukuk structures within the FinTech Lab framework.

Smart Sukuk structuring involves using smart contracts to automate profit distributions, principal redemptions, compliance checks, and event-driven actions (such as early redemption or defaults) within a tokenized sukuk framework, while maintaining full Sharia compliance.

Saudi regulators and banks require controlled, identity-verified environments. Permissioned blockchain architecture for banks ensures that only KYC’d participants can access the network, regulators maintain observer access, and all transactions remain auditable and compliant with CMA/SAMA standards.

Automated Sharia compliance monitoring uses on-chain rules and AI-driven analytics to ensure that tokenized sukuk transactions conform to Sharia requirements. This includes pre-issuance checks, transfer-rule enforcement, and continuous monitoring for anomalies that might circumvent profit-loss sharing principles.

Webmob provides full-stack development capabilities for building permissioned blockchain systems, implementing ERC-3643 token standards, developing automated compliance modules, and integrating with banking and settlement infrastructure required for SAMA-compliant ledger solutions and white-label real estate investment platforms.

Let’s discuss and plan how we can accelerate your growth. Fill out this form and take the first step towards constant advancement.

We will respond to you within 24 hours.

Access to dedicated product specialists.